Content Reviewed by: Dave Gormley •

September.24.2023 Vertified Content

Sep 24, 2023 | Read Time: 5 minutes

Here we go again. The government shut down is scheduled to start October 1. Federal employees may soon be unsure about when they will get a paycheck. This one could last a long time.

What is the best way to budget for a short term crisis like the government shutdown? As a bankruptcy attorney in Southern Maryland for over 25 years, I know exactly how to manage a budget for a crisis. Things you do now will have a BIG impact on your options later. So be careful!

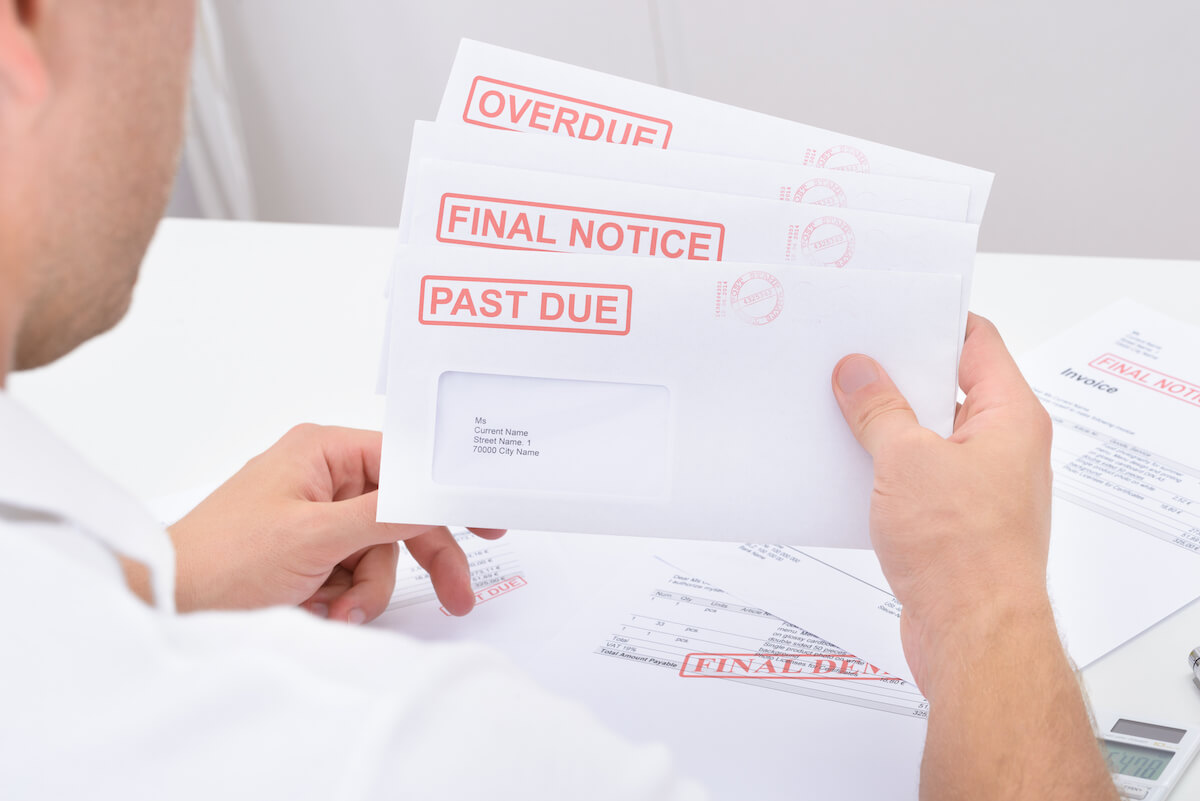

We saw a dramatic increase in bankruptcy filings after the last government shutdown, and the one before that. The same thing could happen now.

The two biggest stressors in life are uncertainty and lack of control. A government shutdown hits federal workers with both of these stressors at once.

You can take back some control of this situation. To do that, you have come up with an emergency budget to get you through a shutdown. Even if you don’t end up using this budget, having a plan will hopefully help you sleep better at night.

Keep in Touch with Your Creditors

First, keep in touch with your creditors. If you do not have enough money to pay all your bills for the next 30 days, call your creditors and let them know. Make sure they understand that you are a federal employee, and you intend to pay your bill when you start getting paid again.

They have a lot of debtors in the same situation, and they may back off collection efforts until the government shutdown is over. No matter what they tell you, it doesn’t hurt to try this tactic. If they don’t know what is going on, they will assume the worst.

Figure Out Your Income & Finances

Second, you need to figure out your income and assess your finances. Take a look at what you have in your bank account. This is going to be your primary income until your next paycheck.

Can you get some income? If there is a furlough, you may be able to apply for unemployment. This is especially important to consider if you are a government contractor. Just keep in mind that you probably will have to pay back this unemployment when you receive your back pay. But having to pay back the unemployment is probably less stressful than falling behind on your rent or mortgage.

While government employees eventually received back pay when the last shutdown was over, many government contractors did not. This left many government contractors spending the next year trying to get caught up on bills. During the last shutdown Maryland encouraged Federal Workers to apply for unemployment benefits online.

Where else can you get money? Look at the savings and lines of credit you can access to pay bills. Try not to incur more debt, but at least figure out where you can in case you need to. Do not include your TSP or 401K in these calculations. You don’t want to access these funds unless there is no other alternative. Tapping this retirement money is rarely a good idea.

If you ever get to the point where you think you need to access these retirement funds, come talk to us first. We offer a consultation to anyone facing a financial crisis due to this shutdown.

Develop Your Emergency Budget

After you determine your income, the next step is to look at your bills and figure out how to make this money last until your next paycheck.

Look at your expenses and prioritize them. Remember, this is not a normal budget. This is an emergency budget to get you through the furlough. This means guessing about how long it will be until your next paycheck. If you have the savings, come up with a 60-day plan. If not, at least look at a 30-day plan.

If you have automatic payments set up, you may need to suspend some of these to make your money last. If back pay is granted, you can use it to replenish your savings and get caught up on bills. To help federal employees and contractors, we are offering consultations to anyone on how to handle their bills during the shutdown.

Not everyone’s plan will be the same. You need to do some research and figure out what is right for you. Some good places to start for information and ideas are the federal credit union websites. Some even may have financial assistance programs in place like Navy FCU, or Pentagon FCU.

Prioritize Your Expenses

Figure out what bills you have coming due in the next 30 to 60 days and what money you have to pay these bills. Now let’s figure out how to prioritize the bills.

As a bankruptcy lawyer who is skilled in budgeting to pay creditors, here is the order I came up with. The most important bills are the ones that make sure you can live your life. The second most important will be the ones that are more difficult to catch up later. There are some way down the list that you might think are more important – but they are not really because you can deal with them later. This is important to understand.

Think about whether or not this order makes sense for you, or if you should shuffle the order of some of these items:

- Groceries

- Medical copays you know are due for upcoming doctor’s appointments.

- Transportation (gas in your tank or public transportation)

- Rent

- Car Insurance

- Car payment

- Utilities

- Mortgage Payment

- Credit Cards

First, make sure you have enough money for food. If this is all you have money for, everything else on the list will have to wait. And if you are under medical care, you need to pay the copays to see the medical providers so you don’t lose your health care.

Don’t forget gas money. For most people in Southern Maryland, you need to have gas money to get to work and to get to the store to buy groceries. If you can walk to the store, this may move further down the list.

Most people think making your mortgage payment is your number one priority. In an emergency situation, this may not make sense. In Maryland, it takes over 4 months for your house to go to foreclosure. And they usually won’t even start the process until you are months behind. And you can always save your house by catching up your mortgage payment. You won’t lose it just because you fall behind a month or two. Just let your mortgage company know what is going on.

In emergency circumstances, it makes sense to put your mortgage payment further down the list. Pay utilities and car payments first. They can shut off your utilities or seize your car much sooner than they can do a foreclosure.

If you are renting, an eviction can happen a lot faster than a foreclosure. Rent should be further up the list. Hopefully your landlord will give you some grace in the face of a government shutdown. You should at least ask.

For most people, cable and the internet would be way down the list. However, if you telecommute, you may want to move your internet service a little higher on the list.

Paying off credit card debt is usually dead last. You need money to live now. You don’t know how long this will last. So don’t throw money away for debt incurred in the past during this emergency budgeting time. You can always deal with the credit cards later. Remember, this is crisis budgeting – not normal budgeting.

Also remember, we offer a consultation to anyone affected by the government shutdown. We can go over your personal finances and work through some good options.

Conclusion

Nobody knows if a government shutdown will last a few days, a few weeks, or longer. Nobody knows if federal employees will be paid for the time they were off due to the shutdown. You should hope for the best, but prepare for the worst. Take action now, and make a plan that gets you through the next 30-60 days. Then keep your fingers crossed and hope this shutdown ends soon!

Want to know more? Discover what you need to know about bankruptcy in Maryland. Click here to see our Free Legal Consumer Guide to Maryland bankruptcy cases and get answers to your questions today. Know your options. Be informed. Protect yourself.

Need a bankruptcy lawyer? Please contact us for a consultation today if you need a Maryland bankruptcy lawyer for your bankruptcy case.

Like our blog? Subscribe to our email newsletter and stay informed!